Sizing a cash position?

"Active" cash on the sideline

“It takes character to sit with all that cash and to do nothing. I did not get to where I am by going after mediocre opportunities.” - Charlie Munger

“The most important quality for an investor is temperament, not intellect.” - Warren Buffett

With markets at all-time highs and constant commentary about how overvalued the market is at present, I have been trying to think through how to effectively build out a cash position to help manage risk. By any valuation metric you look at, valuations are historically high (and only getting higher following Trump’s presidential win). That is not really up for debate, but the question is what to do about it, if anything? I wanted to write this partly because I am unsure myself, but am in the process of developing a strategy and mindset for how to balance risk adjusted returns.

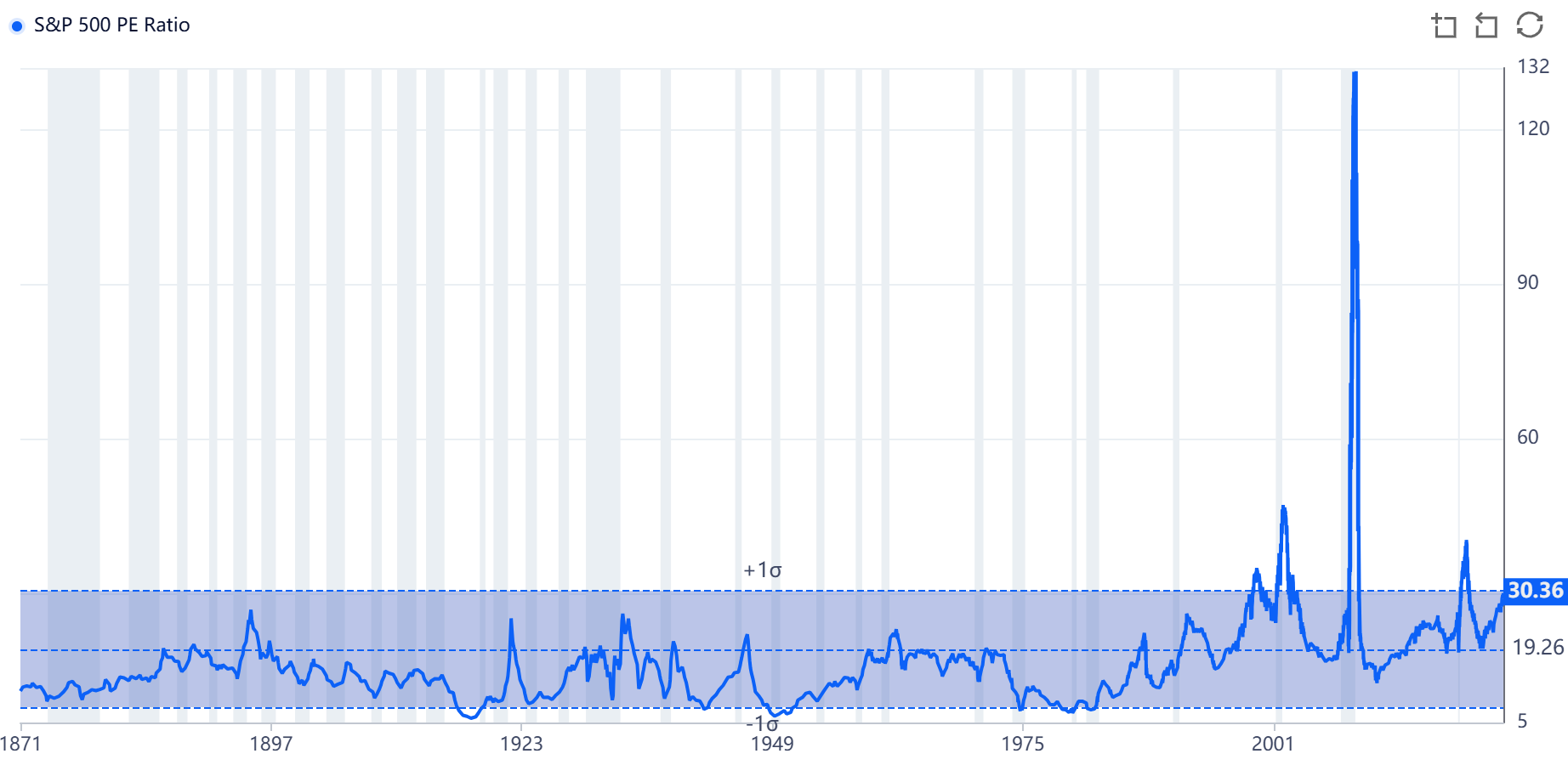

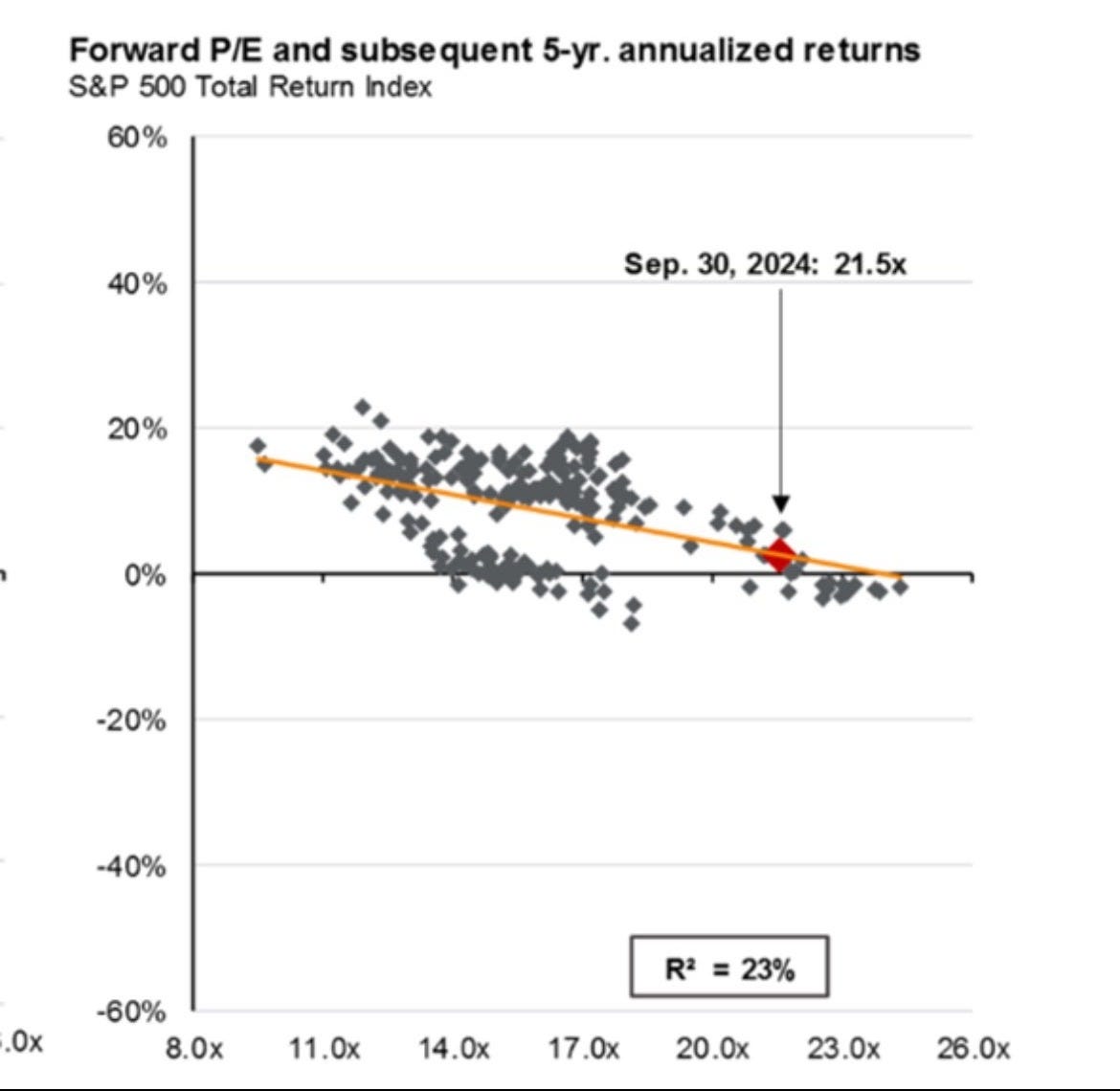

The market is currently priced at 30 P/E (using ttm earnings). This is more expensive than anytime in the last 40 years outside the waning years of the late 2000 tech bubble. Yes, you read that correctly. Goldmans Sachs recently released a report that forecasted the S&P 500 to deliver an annualized nominal total return of 3% during the next 10 years.

It may be difficult to believe given our current climate, but there have actually existed times in history where cash actually has outperformed the market, i.e., 1965-1981 and 1997-2010). Stocks always win out in the end, but valuation always matters! In one sense, I understand that the market will spend a lot of times making new highs. Another sense, I also recognize that cash is more often than not a drag on portfolio performance. This is one of the many great dichotomies of investing. There are a confluence of variables. All I can do as an investor is to weigh risk and adjust accordingly. Current market conditions make it seem very prudent right now to at least take some level of risk off the table, especially considering cash still generates a meaningful yield (>4%). This is not me attempting to make a great market call, this is me as an investor carefully evolving and adapting my strategy to account for probabilities and risks in the market.

")

“Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.” - Peter Lynch

Overall strategy

How do I wrestle between investing in high valuations and cash being a drag on a portfolio? A core tenet of my investing philosophy is to be as close to fully invested as I focus on individual companies over a multi-decade horizon. I am still under 40 (barely) with a high risk tolerance invested solely in equities with a goal of maximizing total return over a very long time horizon with a steady income stream. You can never go wrong with passive index investing in the long run, even if at times (possibly now), the index becomes overvalued and overconcentrated, as it still remains as a wonderful low cost aggregator to compound your wealth over time. Dollar cost averaging into the index will remain a core principle of my strategy to help provide solid ballast when times are tough. One just must accept that current expected returns should likely be adjusted lower, but if you are investing for the long run, then maybe this does not matter as much to you.

Rather than worry about whether now is the right time to buy, just keep buying. Market high or market low, just keep buying. You should think of buying investments like you buy food–do it often….Just Keep Buying is an aggressive investment accumulation approach that will allow you to build wealth. Think of it like a snowball rolling down a hill. Just keep buying and watch that ball grow. -Nick Maggiulli in “Just Keep Buying”

The absolute most important part of my financial goal is to make it to the end, not as quickly possible, but enjoying the journey. This means that there will be times to carefully balance risk and even protect the downside, while also positioning myself to be ready to pounce upon opportunities that the market will inevitably present at undetermined junctures. This certainly does not mean being overly macro fixated or a market timer, but it does mean being macro aware and continuously weighing valuation risk throughout my investable universe. All investment evaluations should begin by first measuring the amount of total risk as it always matters what you pay for a company.

Numerous studies do bear out that cash has proven to be more of a drag on investors’ returns and macro timing is a near impossible quest. Markets will often increase over time and I am a long term optimist in the economy, America, capitalism, ingenuity, and productivity. Timing the market and trimming my holdings are not major theme of my personal strategy as I would rather simply dollar cost average and ride the tailwind of secular growth. Sure, at times the market will be overvalued and at times the market will be undervalued, volatility is par for the course as there is seldom an equilibrium to market emotions.

“Time in the market is more important than timing the market.” - Ken Fisher

My objective is to be a net buyer of businesses over times and allow my winners to do the heavy lifting for me. Post the Great Financial Crisis in 2007-2008, some investors sat predominantly in cash clamoring that the economy would further deteriorate, however, we have now been in an incredible secular bull market and enjoyed one of the greatest 16 years of returns in the S&P 500 history. How painful must it feel to miss out on that growth and still be predominantly be in cash?

No one foresaw COVID-19 in 2020 followed by a stock market bubble in 2021, and everyone was positive of a recession in 2022, only for the stock market to quickly rebound in late 2022.

Perfect market timing is a loser’s game. I remember seeing numerous S&P 500 price targets for ~$4,000 in 2023, today in 2024 we are at $6,000.

Current conditions

In investing, there are always two sides to every coin. Now I am no market timer, but I am market aware as I seek to buy quality companies at a reasonable price. So how do I reconcile being fully invested amidst a pricey market? As my experience builds, I want to develop an optimal strategy that enables me financial and mental flexibility to build out a small cash position, while still being predominantly fully invested. I am looking more in the range of cash as a 1%-10% position and how to think through putting new cash to work. I do firmly believe that there are always opportunities in undervalued stocks or sectors in the market that you can find if you are working hard enough.

Valuations off the top of my head: Small caps > Large caps; Non-US > US; Consumer facing > Semiconductors; Companies with depressed earnings in tough cycles, industry downturns, temporary dislocations (look at yen carry trade unwind), etc.

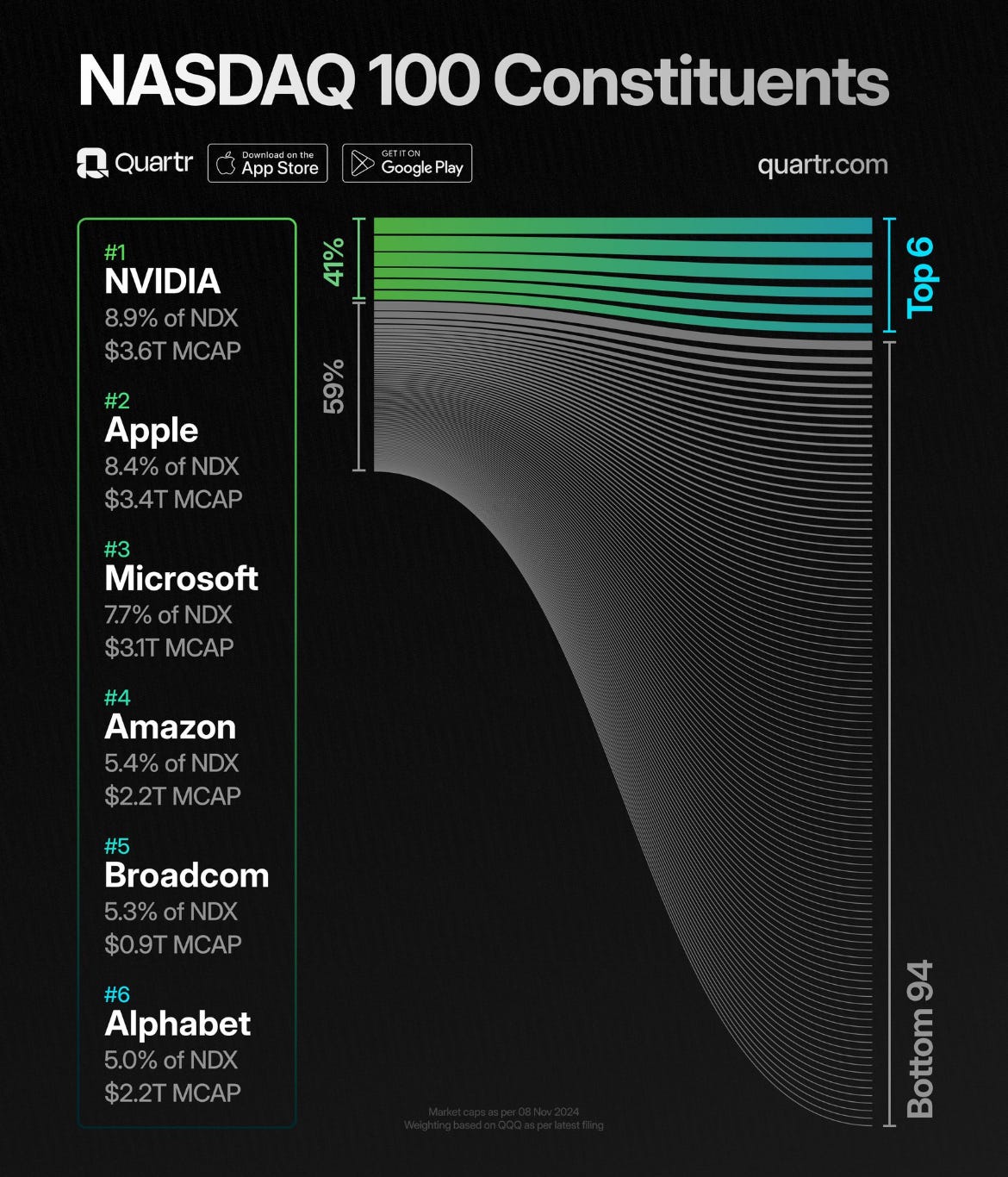

Even now, the market is not quite as overvalued as it first appears as the concentration of top stocks appears to be “holding” the market up. Drilling down even further with Mag 7 stocks, there are vast valuation differences within this group (compare NVDA => 21.7 EV/Sales with GOOG => 5.4 EV/Sales).

However, when I see stocks like Palantir PLTR 0.00%↑ at an EV/Sales of 42 (!). FICO FICO 0.00%↑, is a high quality business, but has a TTM P/E of 114 (!) and only growing revenue in the single digits. My risk antennae perk up.

As of Q3 2024, Warren Buffett and Berkshire Hathaway increased their mountain of cash position to $325 billion(!). Berkshire is clearly defensive as they own more short term US Treasury Bills than the Federal Reserve! What does this mean for me and my strategy though?

While I am obviously playing a vastly different game than the giant conglomerate, I am left with a similar question of trying to strike the optimal portfolio balance by hedging my risk so that I can maintain a cash position to hopefully deploy at lower risk valuations. As I mentioned in “A Falling Knife,” multiple compression can be a major drag to performance. Sound investing really comes down to probabilities and risk. Risk is currently highly elevated, so my reaction is to size my bets accordingly. I am not making a giant market call, but to ignore risk altogether would be reckless.

While I fully accept market volatility, and that my portfolio will inevitably fall at many points, how do I also hedge to protect my downside risk and carefully turn my cash into a position of strength while at the same time not allow cash to materially drag my performance down? A top criteria is to invest in companies with great and healthy balance sheets, so why would I also not seek to obtain a great balance sheet first for myself? In 2022, I remember seeing posts and videos on investors who were taking 50% to 100% cash positions after the market had already drawn down. Market downturns are actually the time to aggressively deploy cash, not build cash, as market valuations quickly move from overvalued to fairly valued to severely undervalued. Currently, I am focused on the other end, when the market has risen so high that it actually becomes sensible to maintain some cash as a margin of safety. Take caution when you see every investor start to post their portfolio returns!

“I have found it wise, in fact, to periodically turn into cash most of my holdings and virtually retire from the market. No general keeps his troops fighting all the time, nor does he go into battle without some of his forces held back in reserve.” - Bernard Baruch

I admit the above quote is a bit extreme, and I certainly do not advocate to moving to 100% cash or anything close to that magnitude, however, I agree with the mindset of viewing your cash as a weapon. You do not always need your troops fighting, and when times do get tough, how reassuring is it to have the reserved fortitude by deploying your “troops” aka cash into the turmoil. Another psychological metaphor I was thinking about is a good campfire. Nothing is better in my opinion! Most of the time the fire burns comfortably within a given range, but when it starts to dwindle and you run out of firewood to add, that is a deflating feeling as you know the cold is coming. Psychologically, it is extremely comforting knowing that you have a steady wood supply ready to add at consistent intervals as needed to help the fire continue to burn long into the night.

I do not mean putting cash aside and not tracking it, but instead really activating your cash position. To me this means knowing the current yield you are earning, the cash balance you are wanting to carry in relation to your portfolio size, and actively searching for deals as they emerge. This could mean quickly deploying into a stock if there is a great short term opportunity or slowly scaling into a position as the risk/reward slowly drifts into more favorable territory.

“To avoid losing money in bubbles, the key lies in refusing to join in when greed and human error cause positives to be wildly overrated and negatives to be ignored. Doing these things isn’t easy, and thus few people are able to abstain. In just the same way, it’s essential that investors avoid selling—and preferably should buy—when fear becomes excessive in a crash.”

― Howard Marks, The Most Important Thing: Uncommon Sense for the Thoughtful Investor

Quick exercise

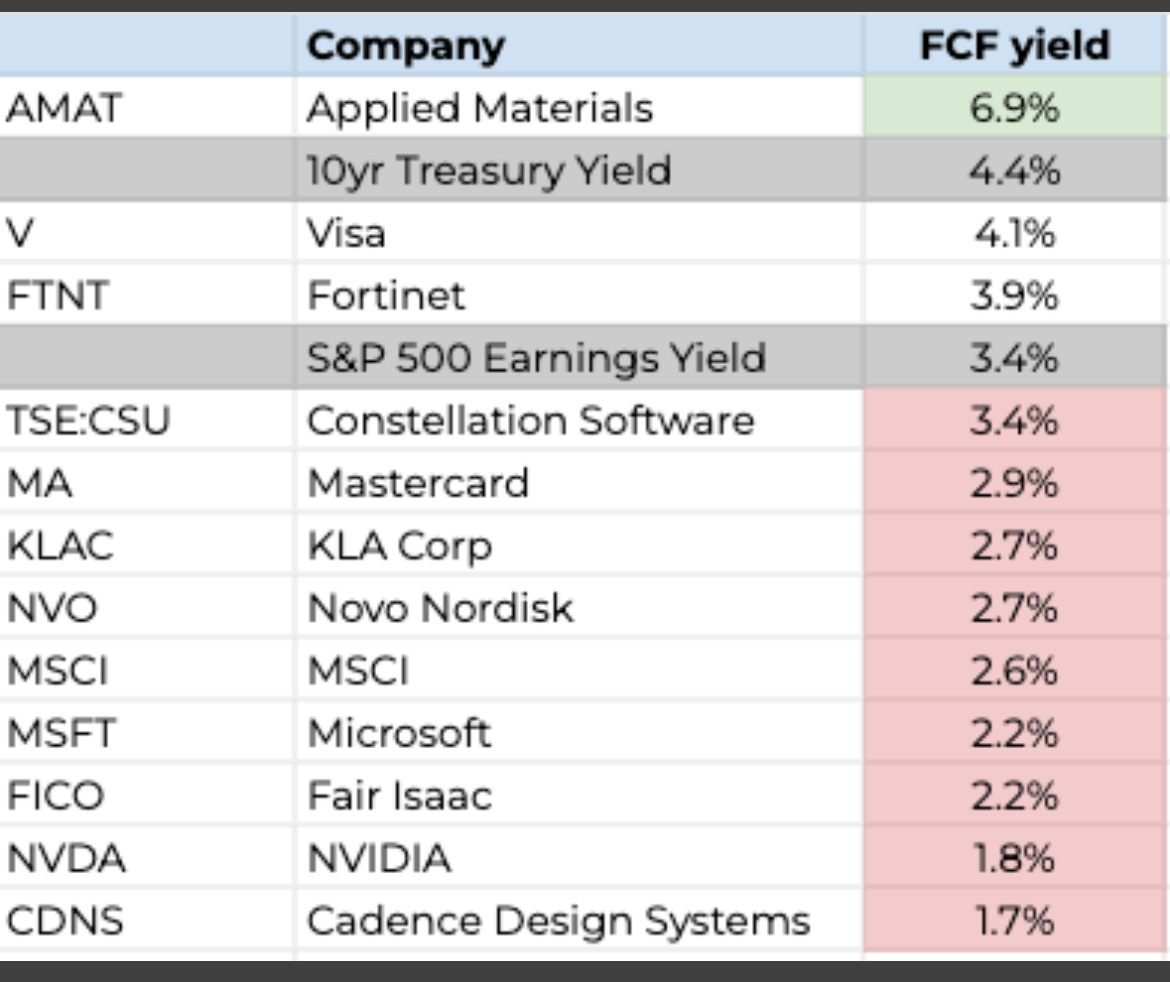

Now we do not know what exact opportunities the market will present and certainly not when, but we do know they will come in some shape or form, and we need to be ready to act on them accordingly. Now the question to consider is what return am I earning on that cash and what valuation risk am I entering into if I buy? Short term treasury yields are still currently over 4%, so the question is, “Can I beat that risk free valuation and at what yield does it become worth it to take on the additional equity risk?” One simple strategy is to chart out the current yields of your portfolio and watchlist (using FCF).

This is just one check that gives you a starting point of being aware of the valuation risks of your holdings compared to cash (10 yr treasury yield) and the index (S&P 500 earnings yield). Based on this chart, one could conclude that Applied Materials AMAT 0.00%↑ may be worth researching more and that the 10 yr treasury yield is still a very attractive place to park cash risk-free until the FCF yield on other holdings rise in comparison. There are many other factors to further dive into, but this is a helpful quick visual to see where your cash yield ranks in terms of equity risk in your total portfolio.

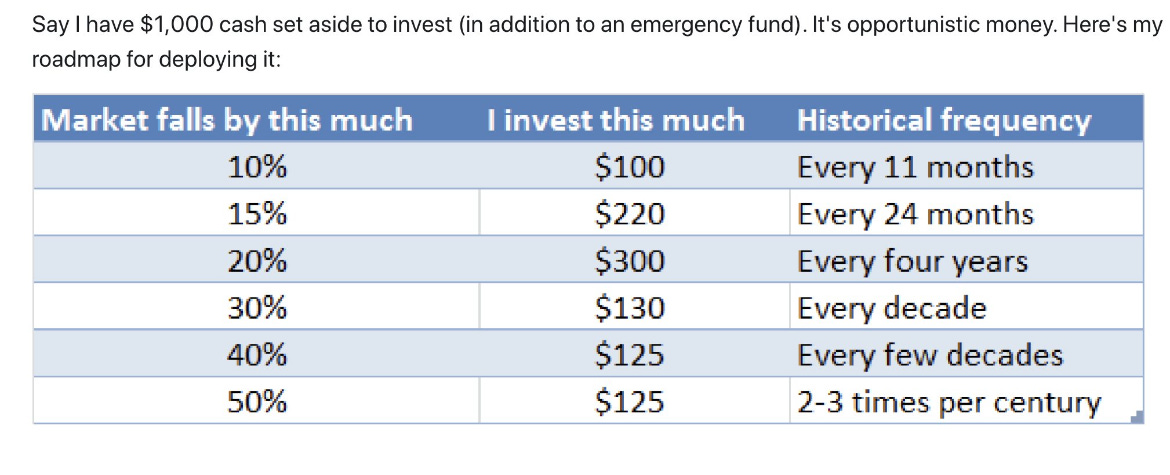

Having a strategy beforehand is imperative to be prepared for inevitable market downturns. We all know the Mike Tyson quote that “Everyone has a plan until they get punched in the mouth.” Well, guaranteed that the market will punch you in the mouth. We do not know when or how these punches will happen, but history is a useful guide to determine that there will certainly be times when the market will assuredly fall and fall fast. The market takes the stairs up, and the elevator down. As investors, we want to be prepared to operate from a position of strength rather than a position of weakness, i.e., selling or accumulating at stretched valuations in order to generate a small cash pile to deploy into lowered risk valuations. Compare this approach to leveraging up in good times to “chase” returns despite elevated risk patterns and then having to sell stocks after they have fallen in order to cover a margin call. We need to always seek a margin of safety, because we can be assured that this will indeed be needed.

Below is another example of a strategy outlined, which provides a systematic guide on deploying capital when markets decline and fearmongering sets in. First of all, you are preparing ahead of time, not getting swept up into the euphoria, but developing a layer of protection to ensure portfolio durability. Secondly, you have a disciplined strategy that gives you a definitive guide so that when the noise and doubt are deafening, you can stay the course while searching to capitalize on opportunistic bargains. You can see below that market corrections are relatively normal.

Holding cash is one of those many investing dilemmas that comes back to each individual investor’s personal mindset and behavior. What works for you? When markets hit downturns, what cash level is going to allow you to maintain being fully invested and possibly even double down. What is your true risk tolerance (typically much lower in reality)? Cash can be a great tool and buffer that will help psychologically boost your current state of mind so that when holdings go down, you have dry firewood to add to the campfire. Statistically, recognize that cash will historically underperform stocks and be a drag on your portfolio performance. However, it may grant you the resolve to remain fully invested in a bear market. If you are uncomfortable investing in higher valuations, then cash can absolutely be a useful tool to potentially have.

“I think cash actually is an aggressive strategic asset because it’s one of the few things that rises in value as the market plunges. Its value is inversely proportional to how challenging the environment is.” - Ken Shubin Stein

Here is the differentiating factor: View the cash as an active piece of your portfolio. Passively active. This allows you to view your portfolio holistically and track the specific cash performance. Money is not sitting idly by or mounting too high, but it is a useful weapon ready to be put to work at a moment’s notice when hopefully valuation risks are lowered as you search for opportunistic bargains. My investing is a journey, and not a sprint. Cash will be invaluable to help weather storms and stay the course on the journey. In highly uncertain times, there may even be extreme market downturns that will offer incredible opportunities should I be vigilantly prepared to take advantage.

"There will be some incident, it could be tomorrow. At that time, you need cash. Cash at that time is like oxygen. When you don't need it, you don't notice it. When you do need it, it's the only thing you need. We operate from a level of liquidity that no one else does." Warren Buffett

Conclusion

All of the above quotes and tidbits sound really wise, but end up being meaningless unless you put in the work ahead of time and properly develop a cash management strategy. Your cash allocation strategy needs to be tailored to your personality and play to your strengths as an individual investor. When the market suddenly drops, time has already likely run out and your animalistic emotions will then override any residual logic as painful portfolio losses kick in.

We do not need to be precisely correct when carrying cash, only directionally accurate. You do not need the perfect cash allocation or always tinkering, only to analyze market risk and sentiment and then size your positions accordingly. Business and investing are ever dynamic with continually changing odds and multiple possible outcomes. There is both skill and luck involved. When stock prices go up it looks and feels great, conversely the valuation risk is also increasing (assuming multiple expansion), which diminishes our margin of safety. Rather than chase pitches low and away, I would prefer to wait for that fastballs down the middle!

Checklist

Primarily focus on the business fundamentals. How much is performance earnings driven or multiple expansion?

Know your holdings and watchlist in great detail. Be ready for big swings!

Do not try to be a perfect market timer or stock valuation picker. Directionally accurate, not precisely correct.

Have a strategy prepared AHEAD OF TIME for inevitable market downturns. The market will punch you in the face.

Preparation. Discipline. Patience. Passively active! Less activity! Narrow focus! Fat pitches over meager results!