Trust the process

Is Copart an AI stock? No, and that's exactly the point

Well it has been a hot minute since I last posted on here, but between the AI craze and raising a 2 year old, I have not worked up the motivation. Personally, my preference is occasional quality deep dives rather than the quick hit pieces. The current state is we are in the midst of an AI bubble and I am not sure how many people would actually dispute that. This may not even ultimately be a bad thing for humanity, but for non-AI investors it has not been the greatest. While AI is leading to technological improvements that will pull us forward, ultimately it comes with a price tag of overinvestment and the end of the bubble will bring forth lots of investor pain.

From the book "Boom and Bust: A Global History of Financial Bubbles" by William Quinn and John D. Turner, there are 3 essential conditions preset to for the Bubble Triangle.

Marketability: The ease with which an asset can be traded or converted to cash (similar to oxygen in a fire).

Money / Credit: Loose monetary policies or readily available credit that fund the speculative purchases (similar to fuel).

Speculation: The psychological heat where assets are bought with the sole intent to sell them later for a higher price, rather than for long-term value (similar to heat).

Following that criteria, I would definitively say these conditions are currently present and it seems like each week gives us a prime example with the latest being the IPO of SpaceX SPCX 0.00%↑. Now at this juncture, I would venture to say that I am not sure when the bubble will end (my guess is we are somewhere in the middle). Is SpaceX the company doing and going to do amazing things for humanity? Most certainly, YES. Are investors going to make good returns investing in a $2.5 trillion market cap company at 60 EV/S? Highly doubtful. Insert the Nifty Fifty track record from record highs; not great Bob.

This is my first “investing in a bubble experience” and it truly is a wild. Every day there are many accounts bragging and posting ridiculous numbers (solely driven by AI) followed by doomer accounts yelling right back “Watch out!” I am an optimistic person and investor, and so I am thankful for technological breakthroughs, but I am also content to miss out on cashing in on the Microns MU 0.00%↑ and Sandisks SNDK 0.00%↑ of the world because those are not the type of companies that align with my philosophy. The truth is though, when bubbles inevitably come along, this will lead to underperformance by many long term oriented investors. This leads to the following questions which I have been pondering. What do I do with the feeling of underperformance? Do I simply accept it and move on? Learn from it? Do I change my approach to perhaps jump in or position to catch the next secular tailwind? Am I just making an excuse for my underperformance?

As always, I want to be driven by cold hard facts and data, rather than narratives and feelings, so what do the actual numbers say. My initial gut told me that this is a period that I need to keep my head down and continue to focus on the long term fundamentals, but to aid my focus, what do the numbers actually say about long term outperformance?

This led me to a study from Shroders, an asset management firm, that confirmed many of my suspicions that underperformance should largely be expected for a vast majority of the time. In their study, 81% of companies that outperformed the US stock market in the last 10 years went through a period of underperformance lasting at least five years. Just as striking, 41% underperformed for at least nine years.

Now, hear me when I say this is certainly not an excuse for underperformance year after year, but this intuitively makes sense. You do have a few market darlings that seem to destroy the market in the long run, but these are few and far between, and even hidden within their outperformance are steep drawdowns that are tough to stomach for investors. Amazon famously fell by 95% in the Dot-com crash, Constellation Software had not had a drawdown of over 25%, but now has recently fallen over 50% despite deploying record high capital. Netflix consistently crashes over 50% and then rises back. Berkshire Hathaway, arguably the steadiest and best compounding stock of our past has fallen over 50% multiple times. Volatility is the price of admission. Drawdowns, hence underperformance in single stocks should be expected at certain times. Why? It could be macroeconomic and sector rotations. Hedge funds have to chase short term performance, which means inherently they need to be momentum seeking and bring capital to what is working today. Right now that is AI, which props these companies’ valuations up temporarily, but also withholds capital from “less favorable” industries. Individual investors do not have to get caught up playing this game, and these short term motivations present long term opportunities.

Other factors could be business reinvestment phases, currently I see Mercado Libre MELI 0.00%↑ fit this description as they are investing $4.6 billion in the Mexican market, which is record-breaking capital for them and represents their largest annual investment in the company's history for a single country by expanding their logistics, advancing technology, and scaling financial services. This fits their playbook and has historically led to very high returns on capital, however…the market just does not look forward and hence has not rewarded this strategic investment. Long term investors, should be beating the table and cheering this long term strategy by management as this is exactly what you want to see. Amazon AMZN 0.00%↑ has followed this playbook and fits this fits this exact mold.

I keep coming back to the fact that most companies possess at least some degree of cyclicality in nature, more than most realize (semiconductors, retail, insurance, food, travel, industrials, etc.). These can face multi-year downturns due to supply/demand imbalances or changing consumer habits. This does not mean they cannot be long term winners still if they have a high returns on capital and forward thinking management, but many will undergo periods of lagging behind emerging industries.

You also have to contend with the law of large numbers as it gets harder and harder to deploy capital at high rates as a company scales bigger and bigger (i.e., Berkshire Hathaway’s massive cash position). Finally, of course you have valuation multiple compression when a stock performs exceptionally well, its valuation often becomes stretched. Even if the company continues to grow profits at a healthy clip, its stock price may stagnate or even fall as the market adjusts to those high expectations back to reasonable levels.

Now, we discussed a myriad of reasons of why stocks may be underperforming, but now what do we with that info. Well, let’s dive into a specific example of a company that I now own thanks to the most recent pullback.

Copart CPRT 0.00%↑

Copart specializes in reselling used, wholesale, and salvage title vehicles, serving various sellers including mainly insurance companies, but also rental firms, municipalities, and charities. This is a wide moat business that has been a huge winner with all time stock performance up a mind blowing 19,736.8%. However, look at this drawdown over the last 3 years down over 50%. And down 15% over 5 years, but still up 370% over 10 years. That is why long term investing pays off!

Now this is painful, but even more painful when we start comparing this to AI stocks that have gone up 1,000% in the last 5 years, but zoom out and Copart has been a tremendous winner. First mistake, we never want to start comparing businesses like Copart to semiconductor or software stocks. We can start to have investment style drift, misread pattern recognition, compromise values, and mistakenly time market momentum. This short term thinking does not end well. We need to dissect each business by itself with its own specific industry dynamics and understand the long term fundamental picture.

Copart has undergone softening insurance volumes as they rely heavily on processing “total loss” vehicles from insurance companies. The company has seen a decline in these assignments because massive insurance premium inflation has led to a growing number of uninsured drivers on the road due to record high costs. Copart does remain sensitive to broader economic conditions, but IMO this has also been an easy excuse by management. Fears of inflation and changing consumer behavior have deterred investors from automotive-adjacent and cyclical stocks especially with the looming threat of growing autonomous driving vehicles. Self driving is a real threat looming, but one that is a long ways away still and more of a narrative risk at the moment. The company reported disappointing Q2 FY2026 results, missing Wall Street estimates with a 3.6% year-over-year revenue decline and a 10% drop in earnings per share, and the P/E ratio went from 40X to sub 20X. Did a mature company like Copart deserve a 40X multiple, maybe not, but is it attractively value at sub 20X, probably so as long as growth eventually returns to “normal.” N

Copart is no longer a high flying growth company, but I often see investors extrapolate low growth to no foreseeable future growth, and I think we need to distinguish between the two. This is a company that has expanded operating margins to high 30s, free cash flow margins to high 20s. They are largely an asset light toll booth (once new land is acquired) operating in a duopoly industry (historically the much more efficient operator of the 2) all while owning over 90% of its own land compared to their competitor (cannot understate how big a competitive advantage that is) and they have their own proprietary auction platform technology. Long-term operator mindset, network effect, physical + digital moat, fortress balance sheet ($4.2 bil cash) ROIC focused, no sexy narrative, no AI hype, no over promise, and heavy strategic buybacks at very reasonable prices. I would say the below is a decent buy signal for long term shareholders!

***Before publishing, I just read how Jeff Liaw, CEO is stepping down and being replaced by Jay Adair. Jay was the prior the CEO and Jeff was only the 3rd CEO in the company’s entire history. The first was the founder and Jay was there since the beginning too. Talk about culture! This does seem to give credence to the concern that the market share losses to Progressive were not entirely driven by insurer market dynamics, but that there has been some mismanagement that could take some time to fix.

Jay started at Copart when he was 19 years old and is only 56 now and has remained Chairman of the Board. He has significant skin in the game ownership wise and is even married to the founder’s daughter. I interpret Jay coming back as a positive signal, but also am cautiously optimistic. He seems like the right person to step back in, but also an acknowledgement that this “turnaround” might take some time. I would expect certain reinvestment and strategic realignment, but they have the cash on hand to ramp their competitive advantage back up. However, we have seen lately though that these “boomerang ceos” have not worked out tremendously well, i.e., Bob Iger (Disney) or Howard Schultz (Starbucks). Adair has been focusing on his family winery business too so hopefully he comes in laser focused and guns a blazing rather than having his focus split two ways. We shall see!

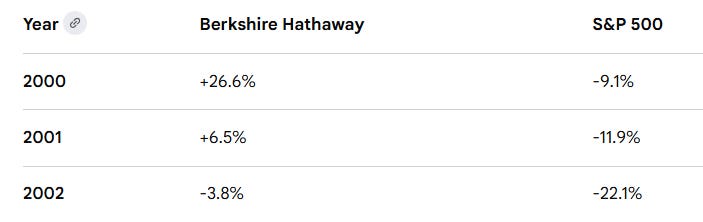

Statistically, it is very hard to beat the market when the market is in a bull market riding a secular trend. For this reason, a low cost index approach is perfectly reasonable and I myself have a large portion of my family’s wealth designated accordingly. My favorite investing book is the The Snowball, which details Warren Buffett’s investing career. The book starts out with Buffett’s ominous warning at Sun Valley at the peak of the dot-com bubble, when he warned an elite tech and media crowd that stock market returns would inevitably lag. The below is the performance of what happens when the air comes out of the balloon.

This is why you do not try to compete and compare on a quarter by quarter basis. You ultimately want downside protection as well, not just moonshots, rather risk adjusted returns. Said better in current terms, when the AI train begins to lose steam, how are your companies positioned. Are their business models completely blown up or barely affected at all? Buffett's presentation at the time was met with heavy skepticism by an audience riding the high of the tech boom, as his value investing philosophy appeared “outdated” to a generation making vast paper profits in internet startups. However, when the dot-com bubble burst months later, his prophecy proved remarkably prescient, wiping out trillions in market value and kicking off a lackluster decade for stock market returns.

Now, where this gets tricky is that as long term investors we want a buy and hold approach, meaning you wait patiently for the right pitch that fits into you circle of competence, you have deep conviction, clears high hurdles into a concentrated portfolio, and you seek to hold to maximize compounding. However, you do not just buy and hold, rather you buy and verify and monitor the business underneath. Numbers themselves are even backwards looking so hopefully you get to the point where you understand the business well enough to determine its future competitive position and whether that position is increasing, maintaining, or decreasing. Easier said than done!

We are in an interesting time where despite market record highs, there are plenty of intriguing opportunities. The Mag 7 P/E ratio is 31 (let alone SpaceX) while the remaining 493 are at a P/E of 20, quite the disparity. As often in the market, the devil is in the details. There are many companies that have been declared AI winners or losers, there are many unloved companies that will simply lag as cycles soften and capital flows to sexier names. The market has become quite disjointed, but this is actually a benefit to stockpickers as opportunities come alive when prices detach from fundamentals both to the upside and also to the downside.

Now underperformance is not meant to be an excuse. The scales will be weighed and balanced eventually (even if it takes a decade), but it may actually take a downturn to be able to really tell the score. We are not in the business of being macroeconomic predictors, sometimes we may just have to suffer the cycle downturns if we are to be left standing victorious in the end. This can only be accomplished by thoroughly understanding the business fundamentals and how despite current cycle weakness, the business is still improving and executing as well as it ever has. I am not sure I can put a number on how long you should expect to initially hold a stock when you initially buy as you do not want to forecast too far out into the future, but I do believe you need to be long term oriented and give your companies enough runway to execute the thesis that you have conviction in based upon your research and analysis.

“The first rule of compounding is to never interrupt it unnecessarily.” - Charlie Munger

#1) The famous “Fidelity study” (coffee can approach) found that the best-performing accounts belonged to people who had either died or forgotten they even had an account.

1. Zero emotional interference

Investors who couldn’t check their accounts avoided panic-selling during crashes and FOMO-buying at peaks — two big wealth destroyers.

2. Uninterrupted compounding

Every trade resets the compounding clock. Forgotten accounts stayed fully invested through multiple market cycles, allowing time to do its work without disruption and large tax implications.

#2) Joel Greenblatt’s magic formula for investing was simply looking at the cheapest stocks at year end that had decent returns of capital. This outperformed for years, which basically was saying the unloved stocks that were thrown out to pursue the high flying names will eventually catch up to at least average. Better risk adjusted returns.

#3) Buffett’s approach switch from one last puffs of cigar butts to durable compounders, but even within this approach he still used independent and critical thinking to discover stocks that the market was clearly mispricing and trading at reasonable starting valuations, i.e., purchasing Apple at a P/E of 10X and trimming it at 30X.

I recently came across a short paper put out by Worldly Partners called General Investing, Discipline Behind 100X Outcomes. They looked at stocks that have gone up at least 100X since 1972 and found that the 82%(!) of those stocks lost more than 50% of their market value at some point, and the average decline of those drawdowns was 65%(!). That’s not the median drawdown for the average stock, that sample size was performed out of 100 bagger sample size. And yet, those companies had returned 533 times on average from their starting point. The other interesting note about that is it was 8 years between highs, which corresponds to the study at the top of this article. That is a lot of active patience, and these were the very best stocks!

Wes Gray authored a piece titled Even God Would Get fired as an Active Investor. He looked back at stocks from 1927 thru 2016 and looked at rolling 5-year periods, and he created the so-called God portfolio. The absolute best portfolio you could create. If an investor with clairvoyant powers picked the best-performing stocks, they could generate a staggering 30%+ CAGR. Despite this stellar return, the portfolio would experience enormous drawdowns (sometimes exceeding 70%), and multi-year stretches of lagging the S&P 500. The fatal flaw is not the strategy, rather investor behavior. Human nature struggles with stomach deep, multi-year slumps, leading them to panic, pull their money, and fire the manager (even God) exactly before the recovery.

Conclusion

I wish that stocks compounded linearly and could just simply grow 15% per annum, but that is not how the market works, however, this is also what presents opportunities. The biggest lesson in investing may just be doing less is often doing more and your biggest edge may simply be getting out of your own way to allow compounding to actually do the heavy lifting for you. You are not going to outperform every year, and that is okay. Your stock may get cut in half and you may have to wait patiently for 8 years; that is not an excuse, but simply a matter of normal stock behavior. Patience, not predictions. There are many forces outside of your control, behavior is not one, you must master this to outperform in the long run.

If you watch the Olympic track events, 1500 meter race for instance, the whole race comes down to that final kick. You have runners who go out and push the pace, while the real threats to win are patiently conserving their energy and positioning themselves for that final burst at the end. The race within the race. What inevitably happens every single time? That winning runner has that big final kick where they are sprinting past and overtaking every runner because all that matters is who gets to that finish line first, and not who was in the lead the majority of the race. Now, this is not the perfect metaphor because there is no finish line for businesses as they can continue to compound your capital for decades to come. There will always be bunnies (currently semiconductor/memory chip stocks, next year ______), but us compounding tortoises will keep compounding along while trends and hype fade into oblivion.

Do you really want to bet that you can find the next Micron and then hold until it spikes? Mohnish Pabrai and Prem Watsa could not hold, why could you? That seems a tough bet to make personally.

There most certainly will be lumpiness and quarters that look better than others, but be sure to align yourself with management who stands behind their words and their actions follow the long term strategy. I know this is totally cheating, but look at the steady compounding cash flow Mastercard MA 0.00%↑ has dumped off (16% CAGR). You could barely even tell this was a worldwide pandemic in there because the business has been that steady.

Investing is simply an attempt to get closer to reality while also not deluding ourselves that we can predict the exact course of a company’s development. For every 100 investors who quote Buffett, myself included, maybe only one can truly follow his advice. Nowhere is this more true than his “no called strikes” idea. Almost everyone cares when a stock they did not buy goes up. It’s called human nature, but if you escape this mental trap, it becomes a superpower. Remember your goals, run your race, no one else’s. Yes, we can all agree that it is exhausting watching investors post incredible returns buying neoclouds and memory chip stocks right now, but just remember when the tide goes out, we will find out who has been swimming naked.

Stay rational in a highly irrational world.

Cheers,

Poor Charlie