Constellation Software update

Is the AI fear justified?

The market is always so dynamic, even though the S&P 500 is near all time highs, there are extreme dislocations in valuations across the board. One main narrative that I find myself contemplating is the drastic rerating of software valuations. AI is the boogeyman, where no one knows the future of just how deeply the rapid adoption will affect companies across the board. My personal stance follows Amara’s Law.

"We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run" Roy Amara

Now, the rate of AI’s adoption and progression has been staggering no doubt, but the true economics and which companies do ultimately benefit are from being determined, yet the market is declaring winners and losers left and right with no room left in the middle ground. I want to hone in on one software company, among the many hit, in particular as this one has become one of my largest holdings, yet is continually being punished by the market for a number of reasons. This post serves as a way where I can step back, thoughtfully examine what the market is saying, key in on business fundamentals, and then make a reasonable valuation determination.

Ouch! I remember when people used to exclaim that Constellation Software (“CSI”) had never experienced a 25% drawdown, which is remarkably rare. Well, now the stock has been taken the woodshed and beaten down like never before in its history. Turns out there were a lot of paper hands holding the stock for the mere reason that “stock goes up.” Well, those paper hands have all been shaken out and then some. First thing first, drawdowns are completely normal and will happen from time to time. Now, there are a few reasons for this and the market is not dumb, but from time to time the market can be extremely manic and increasingly so seems to be momentum driven. Let me dive in to what the market is telling us.

SaaS, as a whole, is getting completely rerated, some deservedly so as valuations were stretched. In essence, the market is punishing incumbent SaaS players due to the fear of potential disruption and the uncertainty about which companies will successfully navigate the transition to an AI-centric world. While some stocks look potentially undervalued based on current fundamentals, many investors are waiting to see which companies can adapt their business and pricing models effectively to the new AI paradigm. There is disruption of traditional models, price compression with generative AI, shift in enterprise spending, and investor uncertainty and capital shift as investors are grappling with the dynamic competitive landscape and the unpredictable return on investment for AI R&D cycles.

The last sentence says it all and explains the rerating of valuations, but basically you can chalk it up to one word: uncertainty. The future is always uncertain and our job as investors is to parse out the risk from the return, and as I will explain later, my analysis is that these fears are overblown. Indeed, a lot of VMS is in trouble. I am no coder or software engineer, but I can understand a full technological advancement when I see one. However, software requires a ton of maintenance. Maintenance and new feature expansion within software is also completely different now. How much will corporations act to build internal VMS solutions and shut off vendors? Some will, sure. It could hurt net new organic, but generally CSI is buying low organic anyways and the cost of VMS is highly fragmented, with tons of customer data, and comprises a small portion of a biz’s budget.

These software bizs (infrastructure, payments, legal, healthcare, public sector, etc.) are deeply embedded in processes, regulation, and decades of accumulated data. Risk of disruption or failure is of much higher importance than minimal cost savings. Switching costs are incredibly high. CSI has 1000+ companies and 1000’s of engineer, and most importantly the trust of 1000’s of clients and 30+ years of domain DATA. That does not go away overnight. The skeptics will not grasp how B2B software stickiness comes from regulatory integration and process reliance, not just the vibe coding by itself.

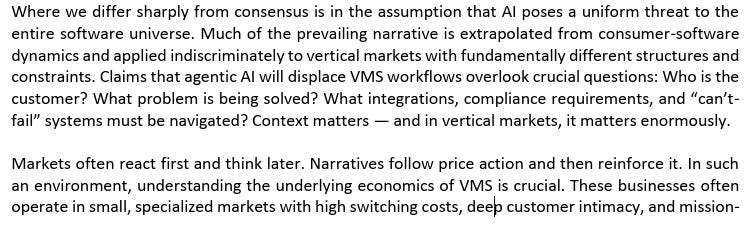

What about all of the ways AI could be a potential tailwind? Will CSI sit around and do nothing or can it leverage AI to lift margins, slows headcount growth, and supports organic growth? Will having more AI projects increases the TAM for acquisitions in the long run? Management has experienced decades of adapting to different cycles (i.e., on-prem to cloud) and have been very proactive to date learning AI. Rerating of valuations could potential enable more affordable acquisitions for CSI to acquire. There is second order thinking needed and various outcomes at play, not just an all software is dead verdict. I would prefer to wait patiently to see how this all plays out as there are many different factors at play. The below excerpt from REQ Capital summarizes the environment and opportunity well:

Source: REQ Capital 2025 annual letter

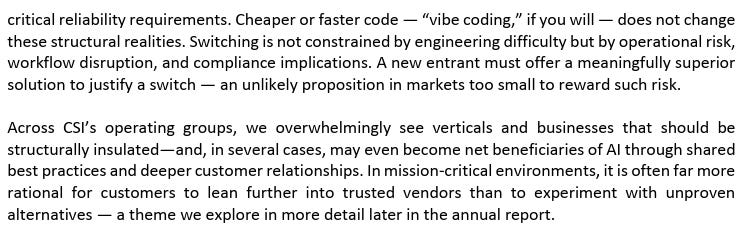

Here is a good post, one of many like it, that further distinguishes CSI’s “system of record” moat from the software code moat. (Click anywhere on the image for the full thread)

The moat is not found in the development costs, rather mission-critical data, complex regulations, deep integration into work processes, and high switching costs.

The sudden departure of Mark Leonard was a huge bummer. He is on the Mount Rushmore of greatest capital allocators of all time and his presence will certainly be felt and missed. The communication scramble and timing certainly did not help the situation. However, he is still Director of the Board and CSI has a long established playbook and track record with decentralized operations. Mark Miller, the newly appointed CEO was the co-founder of the first operating group CSI acquired back in 1995. He is experienced and the playbook does not change overall. The one area where Leonard was great at, similar to Buffett, was he could be very useful in special, mega strategic acquisitions. Overall, similar to Berkshire Hathaway being highly decentralized, CSI has been left in capable hands with a strong culture of decentralization and outsourced decision making.

Now can CSI find the big fish? In time. In 2023, there was a $700 million acquisition by CSI to purchase of the Optimal Blue business from Black Knight. This acquisition was related to a regulatory requirement where the FTC, as a condition of a separate deal with Intercontinental Exchange, required the divestment and CSI savvily stepped forward. Mark Leonard knew how to wield the elephant gun, and Mark Miller will hopefully learn in time to carve out opportunities like these as they will be needed more to meaningfully move the needle. These opportunities come unexpectedly and CSI will be ready when they do.

These are businesses with real moats, durable customer relationships, and most importantly, skilled management teams that have proven their ability to adapt and compound value over time. There is an incredibly disciplined value creation culture that has been built over decades now and has one of the best insider alignment structures out there, albeit it is now being tested in new ways. This culture has cultivated return focused managers with strong allocation mindsets spread across numerous operating groups.

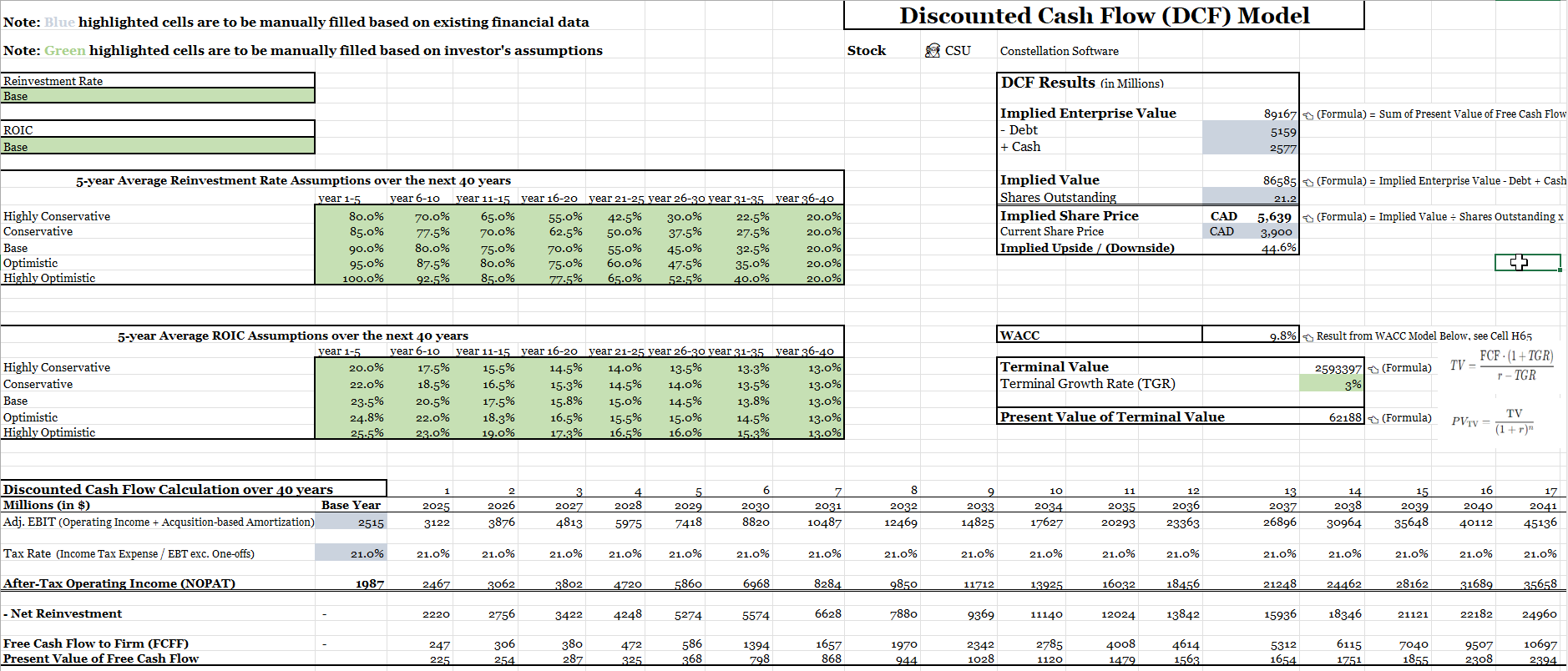

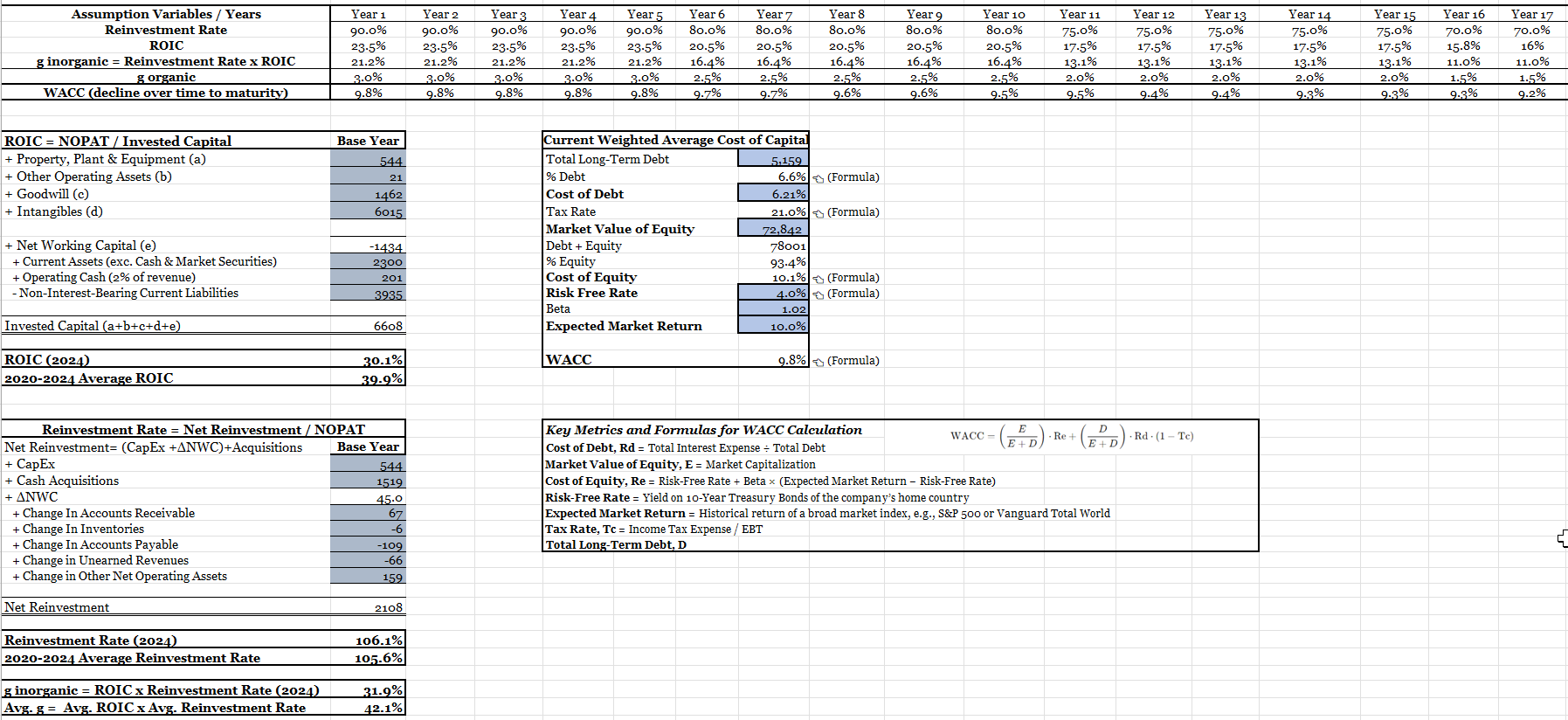

Valuation, everyone’s favorite topic and an important one, but you can boil it down to this: The stock was expensive-ish and now is cheap-ish. CSI takes a lot of work to accurately valu and there are many people that put a lot of work and do a great job. The below is a flawed historical EV/EBITDA metric, but it gives you a quick sense of just how rare this drawdown is in CSI’s history. You cannot simply look at drawdown by itself, but this is a good starting point to dive into understanding what exactly is the risk/opportunity and just how rare it is.

Now, the real question relevant to today is “Is it actually cheap?” Cheap, maybe no (although getting close). Attractive, IMO yes. See below a 5-year IRR sensitivity table that I was looking through.

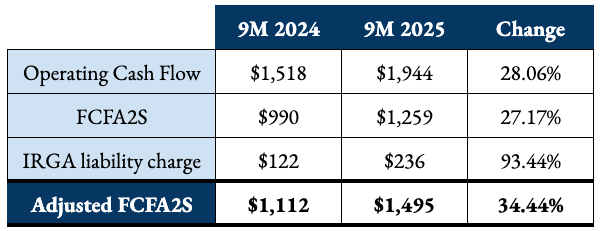

Kip Johann-Berkel@BerkelKipConstellation Software $CSU.TO $CSU *finally* getting to levels where one can make a reasonable valuation argument, imho. ~23x FCFA2S (ttm adding back IRGA liability). Same assumptions as prior post gets you a +13% IRR. I've provided sensitivity table below for other assumptions:

Kip Johann-Berkel@BerkelKipConstellation Software $CSU.TO $CSU *finally* getting to levels where one can make a reasonable valuation argument, imho. ~23x FCFA2S (ttm adding back IRGA liability). Same assumptions as prior post gets you a +13% IRR. I've provided sensitivity table below for other assumptions:

Kip Johann-Berkel @BerkelKipI've yet to see someone buying Constellation Software $CSU.TO at these levels make a valuation argument vs. a "it's down a lot" argument. It's still ~28x FCFA2S! (ttm adding back IRGA liability) If you assume +14% 5-year FCFA2S CAGR and 22x exit multiple that's a +9% IRR5:31 PM · Jan 14, 2026 · 24.9K Views6 Replies · 9 Reposts · 124 Likes

Kip Johann-Berkel @BerkelKipI've yet to see someone buying Constellation Software $CSU.TO at these levels make a valuation argument vs. a "it's down a lot" argument. It's still ~28x FCFA2S! (ttm adding back IRGA liability) If you assume +14% 5-year FCFA2S CAGR and 22x exit multiple that's a +9% IRR5:31 PM · Jan 14, 2026 · 24.9K Views6 Replies · 9 Reposts · 124 Likes

With valuation, your assumptions are everything. Whether you are assuming the multiple gets rerated once the AI fears slow down, or whether you are assuming capital deployment rates decline with CSI’s size, these will determine your investment case for you. So yes, it was very expensive prior to this drawdown, but also this company has one of the most impressive track records of all time.

So what are the factors that really matter that will drive this investment? Not just sentiment and vibes, but cold hard facts. When you do not need aggressive assumptions to assume a 20% CAGR, that is highly favorable outcome as even with a 5% margin of safety that still gets you to a 5 year double at 15% CAGR. I am not sure what will happen with the stock in the next 1-2 years, however, do not color me shock if the stock is trading right back at all time highs in the next 3-5 years. (80% higher from current levels).

The key to any investment is knowing the crucial elements to what makes or breaks the thesis. Typically, these can be distilled down into a few pieces of what truly matters. For CSI, it comes down to total capital deployed and the rate of return on invested capital.

CSI has been deploying record capital in recent years. They are maintaining a high reinvestment rate while creatively deploying increasing amounts of capital. In specific periods, like 2022, the company spent more on acquisitions ($1.6B) than it even generated in free cash flow ($1.3B), pushing the reinvestment rate over 100%. For the first nine months of 2025, the total capital deployed was about 80% of free cash flow available to shareholders (FCFA2S). Contrary to sentiment, business is a booming.

The one thing we know is that CSI is incredibly disciplined with their internal hurdle rate set at >20%. Timing of acquisitions is lumpy, however, I see no evidence that growth is slowing down overall. I would say it is prudent to model a slowly declining core reinvestment rate simply given the company’s size pushing higher and higher. Perhaps growth in FCFA modeled down to 15% rather than historically 20%. That is still 15% growth, better than most all other companies. This is something to monitor, although I do feel these fears over size often get overblown as this fear has been stated for the previous 10 years and will likely be stated for the next 10 years and so forth. Just for simple context, CSI is still just ~6% of Berkshire’s size (different bizs granted) and in my view has plenty of room to grow; at what rate is the question.

CSI’s leadership understands capital allocation and you can trust that management will find creative ways to wisely and strategically invest capital going forward. Throw in the optionality of the spin outs and their success thus far along with continued capital deployment and all of a sudden this adds up to an efficient capital allocation flywheel. I understand that the risk is all about future returns, but just look at the growth in FCFA for a moment and then tell me this is a business with huge terminal risk.

The common narrative that I see is investors claim they would LOVE to buy Company X, however, it remains just too expensive and then the drawdown comes (even for CSI) and then investors pivot and narrative fear keeps them out of buying the stock. Stocks do not draw down for no reason, and sometimes fears do materialize into terminal declines. Can these overblown fears can actually be the door openers that long term investor investors need? Is it scary? YES. Do you know the bottom or when it will turn? NO. Will it produce market beating returns over the next 5 years? If you conclude yes, then you buy.

I keep coming back to Google in my head, but follow the market narrative with that company as an example. Google was deemed an AI loser, falling behind, search disruption, and then all of a sudden everything shifted and it is now clearly the AI winner when the evidence was there all along. The result, Google has gained almost $2 trillion in market cap value in the past year!

Sentiment follows prices not underlying fundamentals.

I constantly have heard many people say how “Google was obvious in hindsight” or how “they should have loaded up on Meta’s stock at the lows” or “ASML was caught in a 5 year down cycle,” yet these stocks rebounded like a rubber band. People forget how psychologically difficult it is to invest against negative sentiment. Lows go lower, bears shout louder, and internally you begin to doubt your analysis. Investors should place heavy emphasis on the future, but often the past is the primary source of how to parse through future info, not headlines. I find the dislocation over market timing to be increasingly true, that Wall Street is focused on the next quarter, yet the long term investor has an opportunity when focusing 5 years out.

“It’s better to be approximately right than precisely wrong.” - Warren Buffett

My learning lesson: Once again, I was too quick to dive in against the downward pressure and bet too early on the stock retreat. I need to improve in my patience and discipline in my own personal capital deployment, however, I cannot be perfect either. Part of me accepts this outcome while another part recognizes that I have an anchoring bias to contend against. I need to do a better job at recognizing just how volatility and momentum driven the stock market has become. My Evolution analysis was largely wrong due to the fact that the business itself and its operating industry were facing severe structural headwinds, not simply the “narrative” around it. There was much more credence to the slowing growth and I miscalculated the threats as short term rather than long term. A painful lesson learned, but learned I sure did.

CSI is a different situation to me in the sense that this fear seems much more “narrative” driven than “structural” like Evolution. CSI washed out the paper hand holders quickly and the the stock has subsequently spiraled since then. I know the company well and have long admired the management, structure, and quality, and believe it has one of the strongest moats out there despite the AI threat. Here’s the catch: If you aim to invest in the highest quality compounders, then you likely need a “fear” or “shock” in order to justify the valuation. The stock traded on the high premium side, and perhaps needed a valuation reset, but this is a gift to long term shareholders as the ‘convenient’ AI narrative will eventually subside and business fundamentals, and more importantly capital allocation will continue to be what is truly driving the wagon as it should be.

There are risks to of course monitor: 1) ROIC drift with size 2) Competition 3) Cultural drift (leadership post Leonard) 4) AI disruption. This is certainly not an investment without risk, no investment is, however, at these levels I do feel confident that CSI will produce a market beating return as FCFA continues to compound mid-teens and the multiple rerates/settles at a higher level than today’s once the AI narrative stabilizes. I always ask, “If you did not have a stock price or financial news to follow, how would you evaluate a company’s position?” Simple advice is often the best so here is my reflection.

As long term investors, we need fears like the current one, to present opportunities or else valuations will always stay richly elevated

Investor words and actions often do not align, i.e., preaching long term, but shaken out by short term noise

Simply be a patient, disciplined investor who invests in the long term at reasonable prices

I am surprised at the suddenness and severity of CSI’s recent drawdown, but I view this as an opportunity. Drawdowns are indeed scary, yet inevitable, and many times investing in them leads to the best returns (assuming the moat holds). Surprisingly, with this one I am not all that worried. There will always be people predicting that the stock will continue to go lower and how it is still not cheap. They may temporarily be right, but at the end of the day one has to trust their analysis and buy even if it feels scary. The negative sentiment will likely last longer, I am not sure how long, but companies with outstanding quality rarely trade at these levels for long and free cash flow growth eventually wins out in the long run. It will be interesting to monitor for sure, but one that I feel confident that the durability of CSI’s business model will be proven to stand the test of time.

Cheers,

Poor Charlie

Author notes:

CSU stock $2,800/share as of 1/20/2026

Feeling: Opportunity, small fear with AI uncertainty, but surprised severe reaction. Sentiment is powerful drug. Patience for longer drawdown, but who knows? Wouldn’t be shocked if stock was $6,000/share in 3 years. Adding at current levels. Checking capital deployment. Future spinco coming in ‘26-27?

I would personally argue that it IS cheap now.

It's now trading at 14x 2026 FCF

That means shareholders would get 7% return even if CSU would completely stop making acquisitions and have no organic growth from now on....

Now CSU is expected to grow FCF at about 20% each year for the next 2-3 years at least.

20% growth on 14x multiple... that's 0.7 PEG

It's cheap.

Great article! I like how you mention the proper way to value CSU, which not many people do (shows how little they actually understand given the increased complexity of serial acquirers). One added thing I'd say is that this is a company that few people can actually understand. It's arguably a blackbox, and the accounting is also much more difficult to analyse - hence difficult to argue its clearly in someone's circle of competence. Just gotta trust the culture on this one. I agree with your analysis, let's just see how much more it can drop. I'm fine holding through the drawdown, sentiment will eventually subside. I think we just need some Q results that show they've acquired some more companies to reassure investors.